When your car gets ruined in a wreck, the damage might be minor or severe. Depending on the age of your car, this could cause your insurance company to deem it totaled. You might want to argue with this ruling, but there comes a point when it’s not safe to drive a damaged car.

What Happens After You Sell Your Totaled Car to Insurance?

Most insurance companies deem cars totaled when it doesn’t seem worth repairing. If the estimate a mechanic gives them is as much as the car’s value, they don’t want to pay it. Some states, like Iowa, say the repairs only need to cost 50% of the value, while Texas raises it to 100%. In most states, 75% is the average total loss threshold.

There’s also the possibility that a car, even when repaired by a reputable mechanic, isn’t going to be safe on the roads. The insurance company would rather get that car out of circulation and give you money to put towards a safer car.

You'll Get Paid and/or Get A Replacement Vehicle

Now, what happens next after insurance totals your car depends on state insurance laws. What they usually do is pay you for the totaled car and take the vehicle off of your hands.

Insurance companies will determine your car’s value using a resource like Kelley Blue Book. They’ll make you an offer and, if you accept, you should have the funds in a few days. The insurance company will tow your car, and you’re free to buy a replacement vehicle.

While you’re without a vehicle, see if your insurance company will cover a rental. This might be something that you have in your policy. If the other driver was at fault, your insurance company might bill them for your rental.

In some states, your insurance provider will replace the vehicle for you with a comparable model. This is especially true for new cars because it’s a straightforward process. For older cars, you might prefer to take the money and shop around for a deal.

DMV Issues a Salvage Title to the Insurance Company

When your insurance provider sends for your totaled car to be towed, you’ll sign your car title over to the company's name. They’ll use it to get a salvage title from the DMV.

Insurance Has First Rights to Do What They Want With the Car

Once the insurance company has the title, they might sell your totaled car to a salvage lot or junkyard. They are now the legal owner of the vehicle and will will then try to recoup some of their expenses after paying out your claim.

Things to Know Before Selling a Totaled Car to Insurance

Just because the company deems your car totaled doesn’t mean you have to sell your totaled car to insurance. Consider these options before you make a final decision.

Your Car is Not a Lost Cause

It's worth noting that just because your car was totaled by insurance, doesn’t mean it’s beyond repair. You insurance provider just believes it’s not worth doing so. Insurance companies are trying to make money after all.

So, if your car’s value is $4,000, but repairs will cost $3,000, they won’t think it makes sense to front the repair costs. You might want to keep the car and repair it yourself. You can do this, although be prepared to pay out of pocket and there's a risk that the car might not be as safe or as reliable even after repairs.

You Can Challenge Your Insurance Provider's Valuation of Your Vehicle

You also don't have to blindly accept whatever your insurance provider says about your car's worth. There are two things you can do:

You can contest the insurance company’s decision to declare it totaled.

The insurance company declares a car totaled if the repair costs exceeds the total loss threshold as dictated by state laws.

You can disagree with it being a total loss. To do this, you'll have to present evidence that (1) the repair costs aren't as high as insurance claims or (2) your car is worth more than the insurance adjuster's estimation. There might be some modifications or car enhancements that they had failed to take into account, for instance. Both options will push the repair costs down to a smaller percentage of the car's value that was previously determined.

You can negotiate for a higher settlement offer.

Even if you do agree with your car being a total loss, you might not think what the insurance company is offering you is a fair price.

Do your own research about the value of your car. Check Kelley Blue Book, Edmunds, or Consumer Reports using the make, model, and year of your car.

You can visit also Carfax and enter your zip code and VIN to get a more specific price. Moreover, you might want to call around to local car lots to see what they’d pay for your vehicle. Take this information back to your insurance company to see if they increase their offer.

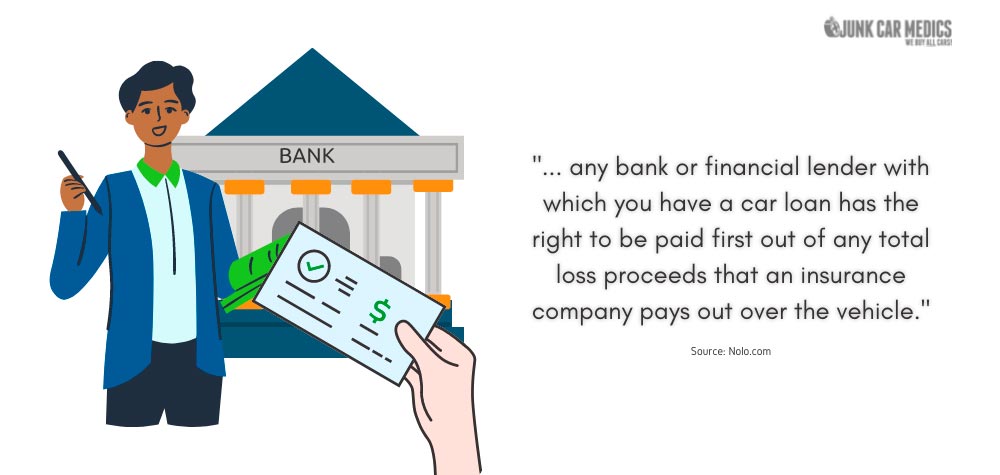

If You Have Outstanding Liens, Both You and the Lienholder Will Get Paid

The insurance company will send the payout to the lienholder since they’re the legal owner of the car. Once they’re paid off, any remaining funds come to you.

However, if the insurance payout is less than what you still owe, you will be responsible to pay for the difference. For example, say that your car is only worth $2,000, but you still owe $3,000. All of your insurance payout will go to the lienholder, and, on top of that, you’ll still to pay them $1,000 in outstanding liens. That can make it financially difficult to find a new vehicle.

But if you have gap insurance, the insurance company will also pay that $1,000 toward your loan. Now you’re free to find a replacement car without an old loan hanging over your head.

You Can Keep the Car AND Get the Settlement Payout

You can choose to keep your car even if it’s totaled. Just tell your insurance provider you want it, and they’ll then subtract the salvage price from what they were going to pay out.

After getting the settlement, you have free reign on what to do with your vehicle. You can choose to keep your car for repairs or sell it yourself to a private buyer, the salvage yard, or to Junk Car Medics.

Final Notes

If your insurance company rules your car totaled after a wreck, don’t feel like you have to sit back and follow their lead. There are many different ways you can handle this situation. You can sell the totaled car to insurance, sell it yourself, or repair it and keep driving.